Continuous Compound Interest

In Recitation 4 we first met the investment as a single number multiplied year on year: the balance at the end of year was , with the assumption that interest is paid once and added to the principal at year-end. Lesson 5AM lifted that model to a continuous-rate equation , and Lesson 5PM named our proportionality constant via the reduction theorem. We’ve suppressed two pieces of the picture so far: a real bank does not pay interest only at year-end, and the relationship between an advertised annual rate and our closed-form constant depends on how often the interest is added.

A bank that quotes an annual rate , written as a decimal, and compounds times per year applies the rate at each compounding step and credits the result to the balance. Increasing at a fixed increases the balance at the end of the year, but only by an amount that shrinks with . The limit of that process gives us the continuous compound formula, and our constant in for that limit is exactly the advertised rate .

Compounding Times per Year

Let pounds be invested at an annual rate of (written as a decimal, so means ), compounded times per year for years. Each compounding step multiplies the balance by , and there are such steps in years.

The compound amount after years at annual rate compounded times per year on an initial principal of pounds is

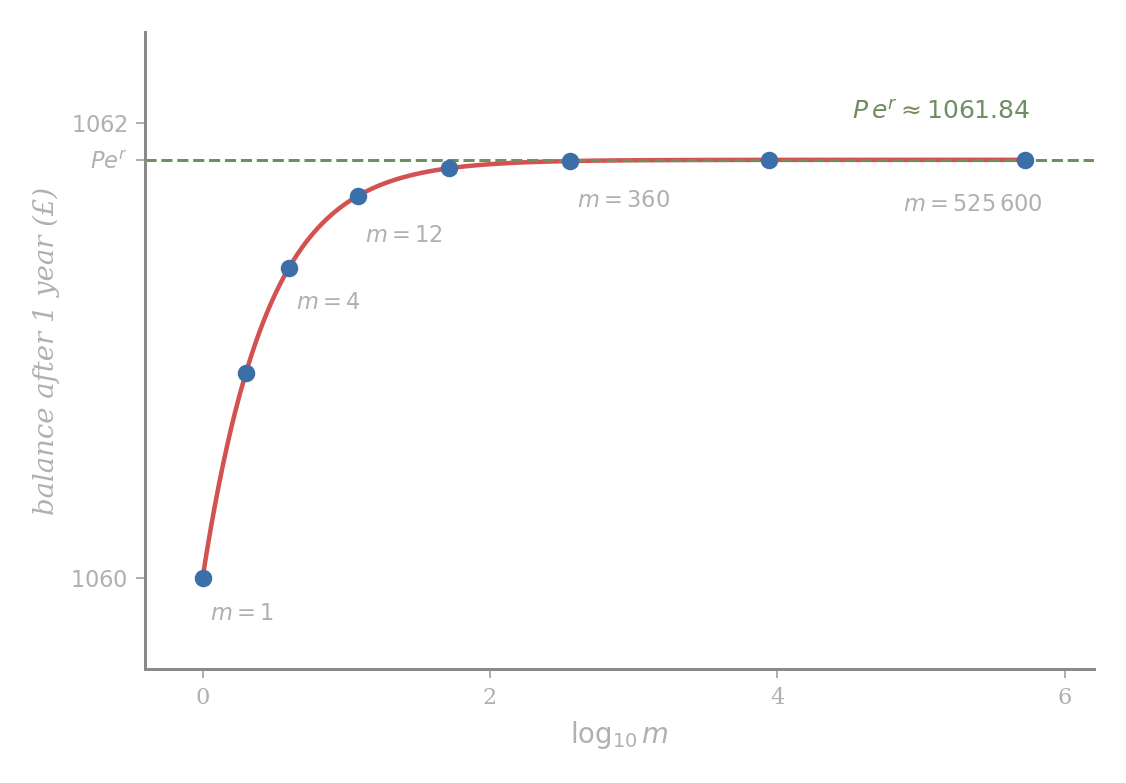

For £ at over one year (, , ), formula evaluated at four common choices of produces the table below.

| Compounding | Balance after year (£) | |

|---|---|---|

| Annually | ||

| Quarterly | ||

| Monthly | ||

| Daily (360-day year) |

The annual figure £ is the textbook simple-interest case. Quarterly compounding adds £, monthly compounding adds another £, and daily compounding adds a further £. Each refinement of the schedule shrinks our gain. The next question is what happens at .

The points crowd toward an asymptote as grows. Going from annually to daily compounding gains £; going from daily to compounding once per second adds less than £. The limit is in plain sight, but a formula for it requires the continuity of and the derivative computation from Lesson 5PM.

The Limit as

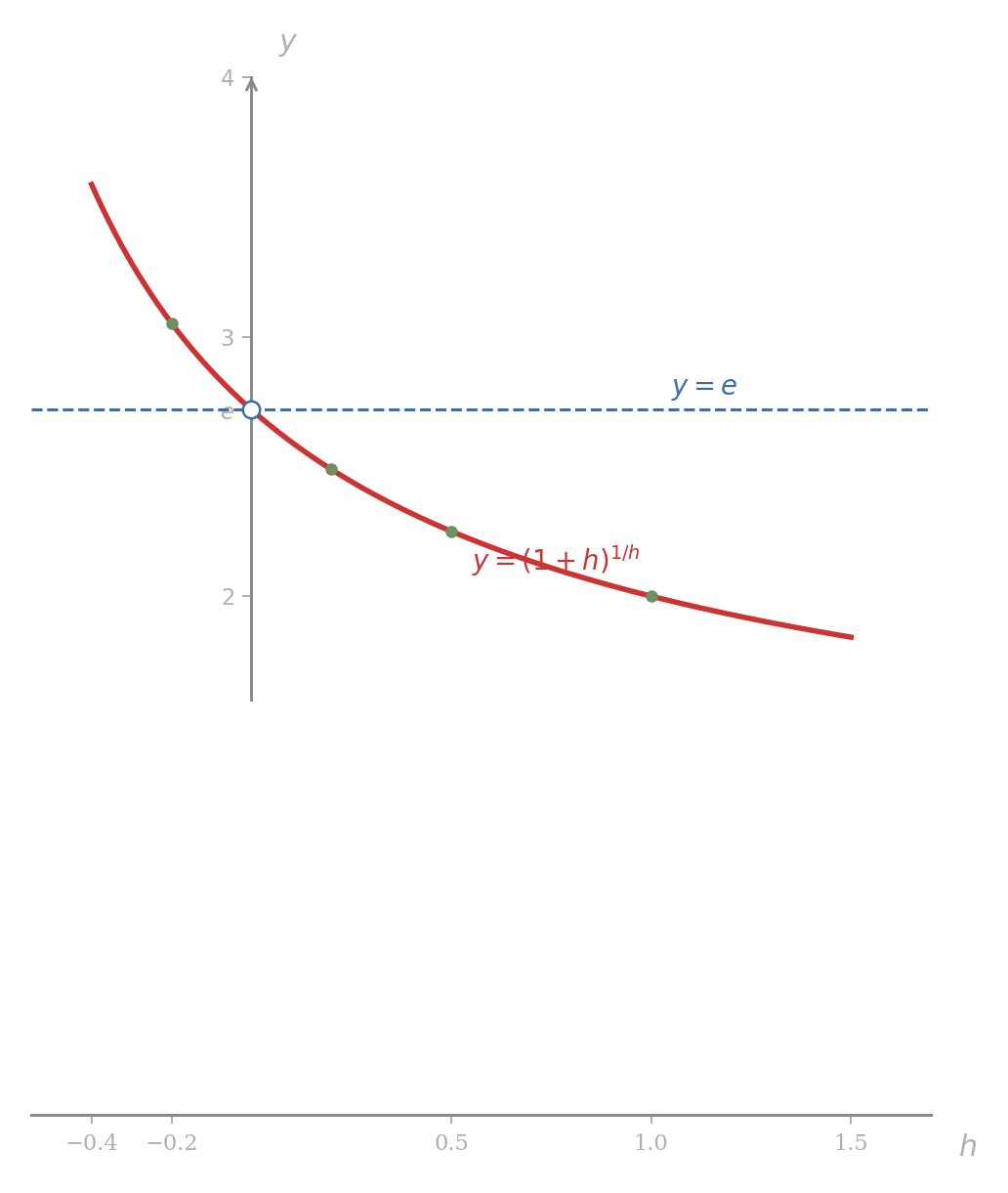

We rewrite to expose the structure of the exponent. With , our substitution gives and so . Then

Sending at fixed sends through positive values, and our limit on the right of depends on the inner factor alone.

For near but , the base is positive, and the real-power definition from Lesson 5PM applies:

Since the exponential function is continuous,

The inner limit is the difference quotient of at . Using from Lesson 5PM,

where the third equality uses the derivative of from of Lesson 5PM. Therefore the inner limit is , and the outer one is .

■

The convergence is slow. At the value of is , well below ; at the value is ; at the value is , still rounded short of in the third decimal.

Continuously Compounded Interest

With in hand, our limit of as follows. Using two of the limit theorems from earlier in the course (the limit of a constant times a function and the limit of a fixed power),

A principal of pounds at annual rate , compounded continuously for years, has balance

The £ at over one year now has a closed-form continuous limit:

This is the upper bound the daily, hourly, and minute-by-minute entries of the table were creeping toward.

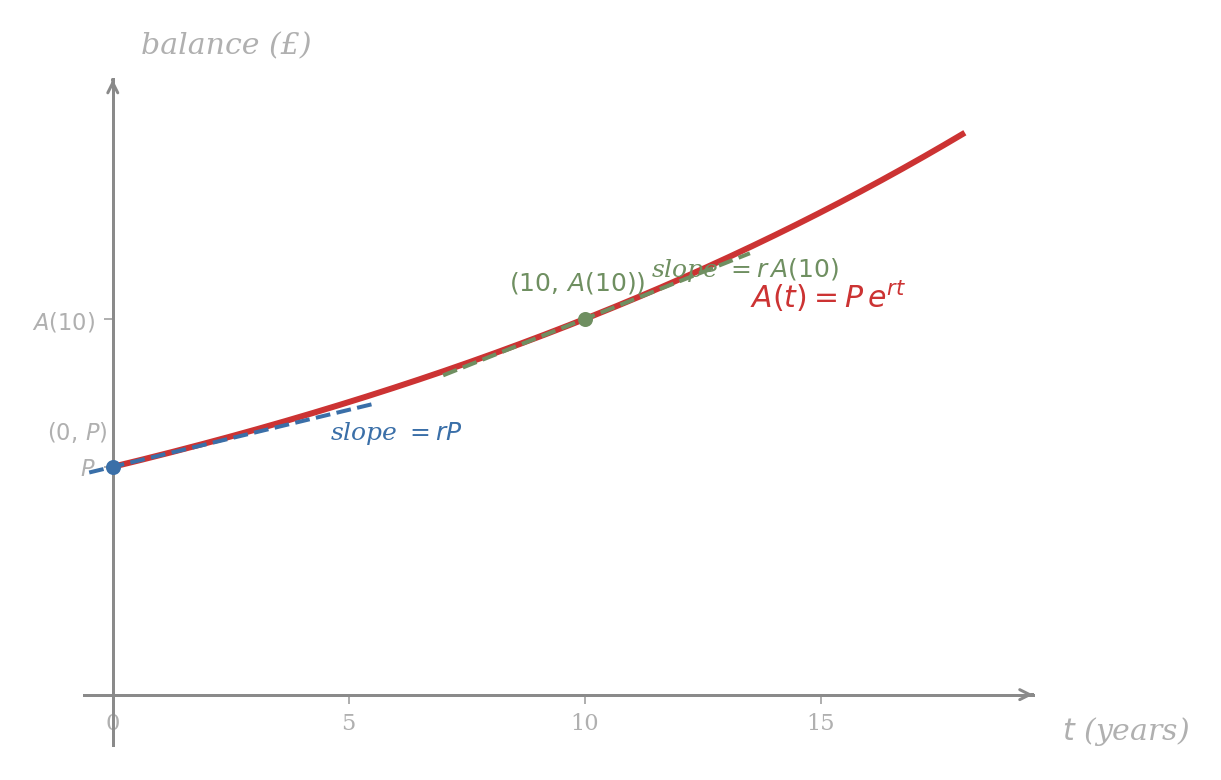

The function satisfies the rate equation

by the formula for . The proportionality constant in the rate equation from the solutions theorem is precisely the continuously compounded annual rate . Interest is being added not at year-end, nor monthly, nor daily, but at every instant, at a rate proportional to whatever is currently in the account.

The slope at is , which is the simple-interest rate per year applied to the original principal: an account paying continuously at percent and an account paying simple interest at percent grow at the same instantaneous rate at . They diverge for because the continuous account immediately starts earning on the new interest.

Recitation 4’s example invested £ at per year, compounded annually. Reset the same conditions to continuous compounding at the same nominal rate, and answer four questions about the resulting account.

- Write the formula for .

By with and , .

- Find the balance after years.

pounds.

- Find the rate at which the balance is growing years in.

Two routes. The chain rule applied to gives , so pounds per year. Alternatively, the rate equation gives the same answer in one step: pounds per year. The growth is in pounds per year because is in pounds and is in years.

The advertised rate is not the rate of growth in pounds per year; it is the rate of growth divided by the current balance. Six years in, the £ balance is itself earning interest, so the growth rate £/year exceeds the £/year that the original principal alone would generate.

- Find the time at which the initial deposit doubles.

We set and solve for :

Taking logarithms by the procedure of Lesson 5PM,

The doubling time depends only on , not on . Had the principal been £ or £, the equation at the doubling time collapses to the same .

The doubling-time computation in part (d) generalises immediately to any continuously compounded account.

A continuously compounded account at rate doubles in time

The doubling time is independent of the principal .

Problem 171

A British saver invests £ at per year compounded continuously.

- State , , and the doubling time, all in closed form involving and .

- Find the time required for the balance to triple. Express the tripling time as times a constant.

- Show that the tripling time exceeds the doubling time by exactly , and rewrite this gap as over using LIII of Lesson 5PM.

Pablo Picasso’s painting The Dream sold in for £, a war-distressed price. In the painting was auctioned for £ million. Treat the painting as an investment growing under continuous compounding, and find the implied annual rate.

We let measure the value (in millions of pounds) of the painting years after . Then million and million. By ,

Taking logarithms and applying of Lesson 5PM on the left,

The painting earned a continuously compounded return of about per year over the -year holding period. Compared to the original Recitation 4 investor at a flat annual return without continuous compounding (so the multiplier is , reaching about £ million on the same £), the painting did roughly times better than the same nominal rate compounded only annually. The inferred continuous rate of corresponds to an effective annual rate , a gap that compounds itself over years.

Problem 172

A British government war bond issued in paid £ at maturity in , after years. Treating the bond as a continuously compounded investment from a hidden purchase price at per year, find in closed form. Verify the closed form against the numerical answer using and .

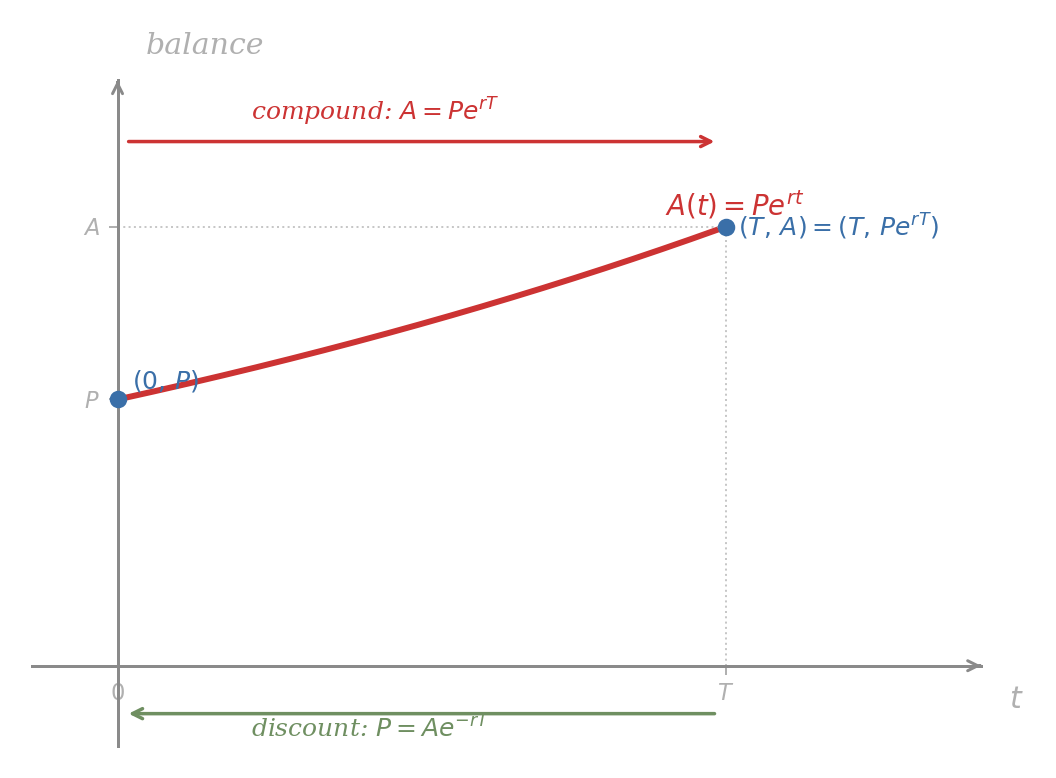

Present Value

Formula takes the principal at time and projects it forward to time . The reverse reading takes a target value to be received at time and asks how much money invested at time would grow into that target. We solve for :

For a future amount to be received in years, with money assumed to earn continuous interest at rate , the present value is

is the unique principal that, if invested at time at rate compounded continuously, would grow exactly into at time .

The present value is what £ at time “is worth right now.” Two payments £ at time and £ at time with are not equivalent at the same fixed amount, because the second can be matched with less principal today. Present value is the standard exchange rate between money now and money later.

Find the present value of £ to be received in years, with money invested at continuous compounding.

By with , , and ,

A holder of £ today, given access to a continuous-compounding account, can convert the present value into the deferred payment with no extra effort: the account grows from £ at to exactly £ at .

A British supplier offers two payment terms for the same delivered goods:

- Offer A. £ today.

- Offer B. £ in months.

The buyer has access to a continuous-compounding account at per year. Which offer is cheaper, and by how much in present-value terms?

Offer A has present value £ by definition. Offer B has present value, by with , , and ,

Offer B is more expensive than Offer A by £ in today’s pounds. Equivalently, the buyer would need to deposit £ today at continuous to clear the £ in months.

The threshold rate at which the two offers tie is the unique with . Solving gives , just above the buyer’s . At any rate above , Offer B is the better deal in present-value terms; at any lower rate, Offer A is.

A common phrasing in finance is that future payments are “discounted back to the present.” The discount factor for a payment at time is , which is strictly between and for every and . The further out the payment, the smaller the discount factor, and the smaller the present value of a fixed nominal payment.

Problem 173

A pension fund must pay £ in years. Money is invested at per year, compounded continuously.

- What present value must the fund hold today to meet the obligation?

- If the rate were instead , by what factor would the required present value change? Express the factor as and compute it to four decimals.

- The fund actually holds £ today at . How many additional years must elapse before the £ alone grows into £? Express the answer in closed form involving .

Problem 174

A trustee must arrange a payment of £ in years. Money is invested at continuous rate . The trustee may also need to withdraw a fixed amount £ at an earlier time , with , for an unrelated purpose; the withdrawal is removed from the account at and not replaced.

Show that the smallest single deposit at that meets both obligations, namely withdrawing £ at time and still having £ at time , is

Explain in one sentence why the right side is the sum of the two payments, each discounted to the present at the same rate.

The Effective Annual Rate

Two banks may quote the same nominal rate but compound at different frequencies. A bank that compounds times per year multiplies the balance at the end of one year by , while a bank that compounds continuously multiplies it by . The convergence figure above showed the latter as the limiting case. The single number that describes the year-on-year multiplier of any compounding scheme is its effective annual rate.

The effective annual rate of a continuous-compounding scheme at nominal rate is the unique for which

Equivalently, .

A nominal continuous account has effective annual rate , so an account quoting ” continuous” actually returns about per year. The gap widens with : at , the effective rate is , and at it is .

A British savings account offers per year compounded monthly. Express the same return as a continuous rate.

The discrete-compounding multiplier for one year is . The matching continuous rate satisfies

Take logarithms by Lesson 5PM:

The continuous rate equivalent to monthly compounding at nominal is about , slightly less than the nominal . The two accounts produce identical year-end balances, since by construction , but the labels differ because one quotes the continuous rate and the other the nominal.

Problem 175

A bank quotes a nominal annual rate of . Compute the effective annual rate under each compounding scheme: annual (), quarterly (), monthly (), daily (), and continuous. Express each effective rate to four decimal places, and identify the gap between the daily and continuous rates.

Problem 176

The continuous rate matching a stated effective annual rate. A British investor sees an account advertised with effective annual rate . Find the equivalent nominal continuous rate , in closed form involving , and verify that the answer is strictly less than . State a one-sentence reason, in plain words, why is forced.

Two Closing Applications

Our next two examples use the same toolkit on settings where the pattern is what we want, not the closed form.

A British investor places £ at continuous rate for years, ending with balance . A second investor places £ at the same nominal rate but compounded only annually, ending with . Show that the ratio of the two balances is

and conclude that the continuous account exceeds the annual account by an exponentially growing factor, with growth constant . Find the year at which the continuous balance is twice the annual balance, in closed form involving .

Our numerator and denominator share the principal , which cancels. By LIV of Lesson 5PM applied to ,

so the ratio is by law (iii) of exponents from Recitation 4. The exponent grows linearly in at the constant rate , which is positive because for every (a fact verified in the next problem from the derivative of ).

For the doubling year, we set the ratio equal to :

At , this gives years before the continuous account doubles the annual account on the same nominal rate. The gap is real but slow, so everyday savings notation can quote a single annual rate without losing any decimal a saver cares about.

Problem 177

(Harder.) Define for . Differentiate once and show for and for , so has a strict relative maximum at . Conclude for every , that is, on , . Use the inequality, applied at , to confirm the positivity of the growth constant in the previous example.

A British contractor offers a phased payment plan for the same delivered goods: the buyer pays £ today, £ in year, and £ in years, for a total nominal of . The buyer can borrow or lend at continuous rate . Find the present value of the entire phased plan, then determine the equivalent single-payment-today amount that exactly matches the plan’s present value.

We discount each payment to the present by :

The first payment is made at , so its discount factor is ; the others use and . Pulling out front gives us

At , and , so

The phased plan with nominal total has present value , a reduction of from the nominal because two of the three payments earn interest in the buyer’s hands before they are due.

The equivalent single-payment-today amount is exactly the present value . A buyer with that amount in hand and access to the account can clear the contractor’s three payments by depositing the lump sum, then withdrawing £ at each due date.

Problem 178

(Harder.) Two competing British insurance products promise the same payout £ in years from a one-time premium today, but at different continuously compounded rates: product A guarantees rate and product B guarantees rate . The premia and are set so that each product just meets its obligation: .

- Express the ratio in closed form involving , and conclude that .

- The buyer’s cost of capital is a third continuous rate . The buyer’s effective loss from committing the premium £ today rather than holding it for years at rate is . Compute the difference in effective losses between the two products, , and show that for every .

- State, with reasons drawn from this lesson, why the buyer prefers product B on every dimension that matters: smaller premium, smaller effective loss, identical payout.

Problem 179

(Harder.) A real-estate investor purchases a London building for £ in year . The market value in year grows under the continuous-compounding model . The annual property-tax rate is a continuous outflow of pounds per year, paid out of the building’s market value. Define the net rate of growth as

- Compute the net rate of growth in closed form. Identify it as a constant.

- Find the condition on and for the net rate of growth to be positive. Express the borderline case as a single equation.

- Using this net rate, express the investor’s after-tax doubling time in closed form as over a single constant.

| Rule | Form |

|---|---|

| Discrete compound interest | |

| Limit formula for | |

| Continuous compound interest | |

| Rate equation | |

| Present value | |

| Doubling time | |

| Effective annual rate |